Stochastic Decision-Making Model for Aggregation of Residential Units with PV-Systems and Storages

Published:

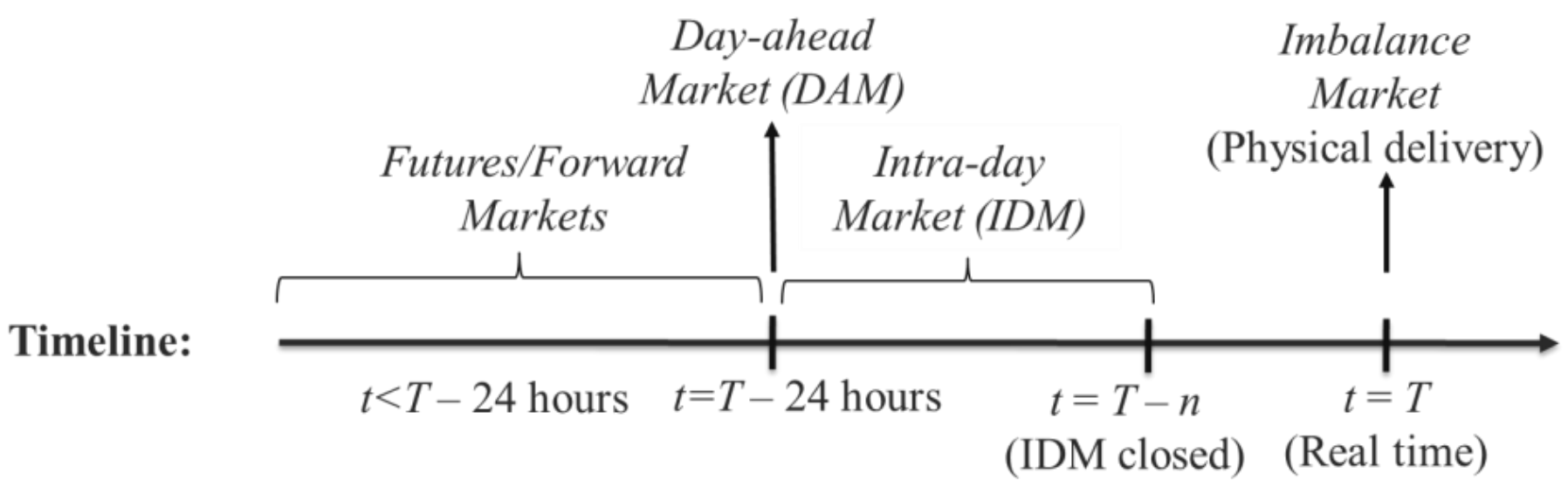

Households are adding PV panels and energy storage to increase their capability in getting lower energy bills. In the following figure we can see a two-settlement market that the household will eventually buy power from.

This market consists of one Day-Ahead market (day -1), and 24 Real-Time markets (day 0). At any point, of time at day 0, the market price and power generation of the PV panel for that hours and previous hours are known, but the same variables are unknown for the coming hours.

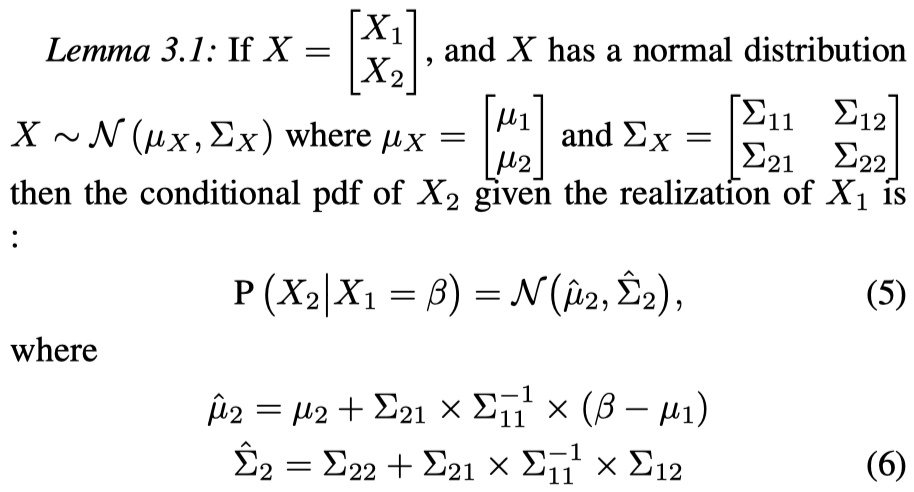

The unknown variables are represented by scenarios. To generate scenarios, we first use Seasonal Autoregressive Integrated Moving Average (SARIMA) to give a single forecast for the unknown variables. We then use the joint probability distribution funciton (pdf) of the forecast errors to generate the scenarios for the forecast errors, and add them to the single foreast generated by SARIMA to create the final scenarios. The pdf we used for the forecast errors is Gaussian pdf, which gives us computational power when calculating the conditional pdf given the new observations.

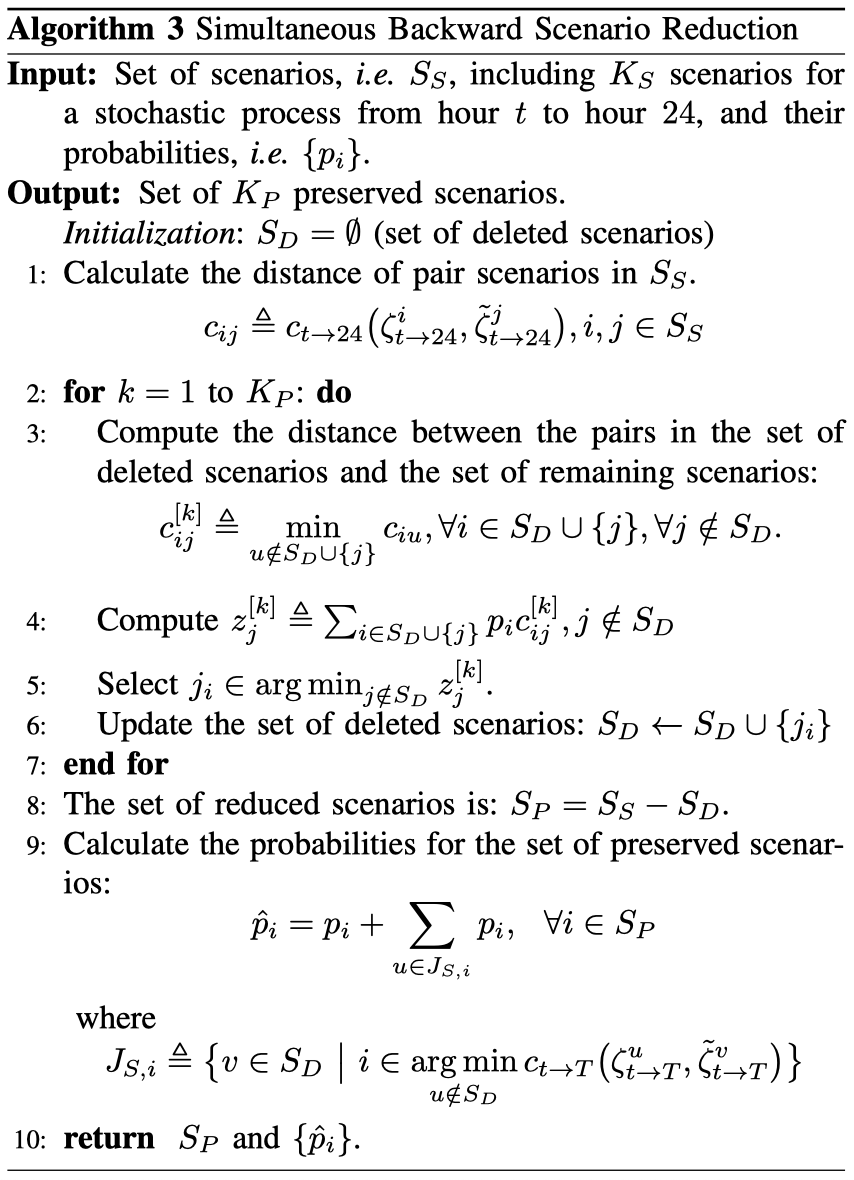

We then use Simultaneous Backward Scenario Reduction to decrease the number of scenarios while trying to keep the most important information in the scenarios unchanged. Then these scenarios are feed into a stochastic optimization problem to generate the optimal decisions.

As we progress into the day, new realizations for the market prices and for the PV power generations come into the light. By modeling the pdf of the forecast errors as a Gaussian pdf, we have a closed form formula for the conditional probability distribution functions of the forecast errors.

To see the pdf of the paper, see link.